The UK’s tax story takes another twist: HMRC is lifting the Income Tax personal allowance above £12,570, but only for people above State Pension age. Working-age earners stay stuck on the frozen threshold. Two Britains, two tax baselines, one uneasy question about fairness.

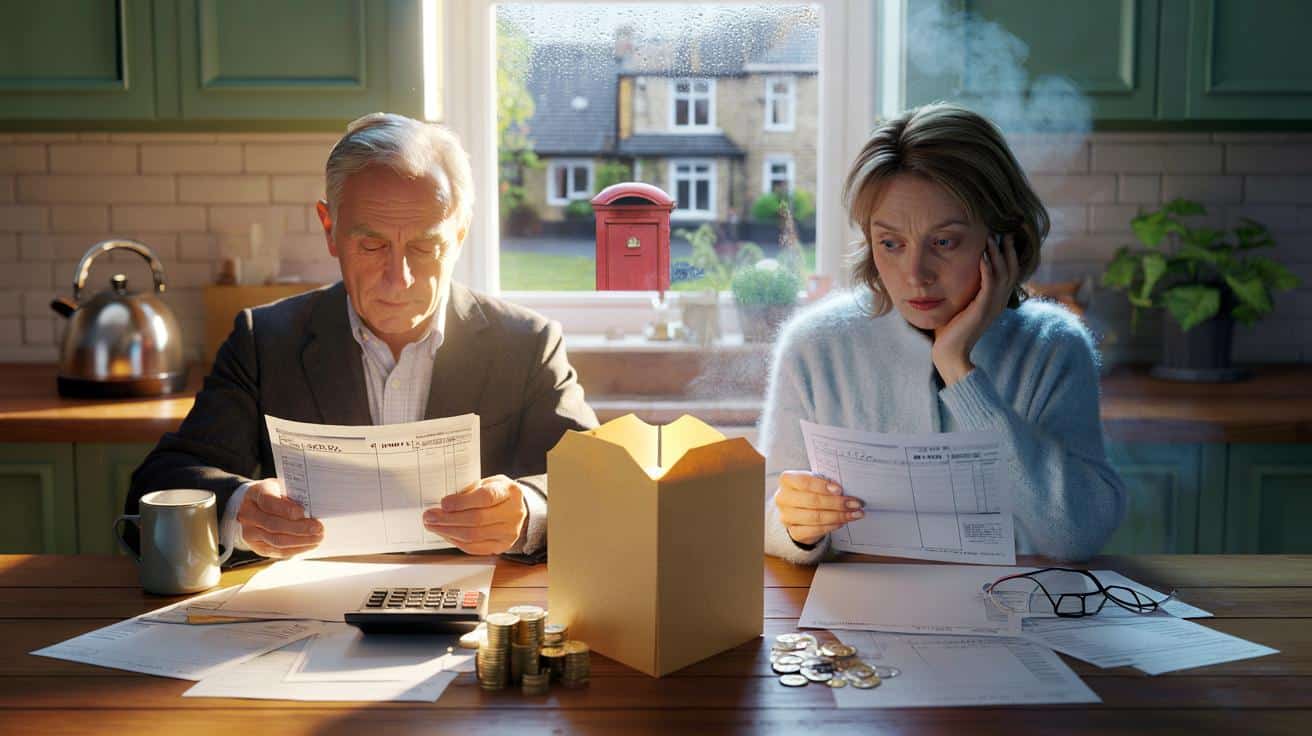

Ken is 69, Maureen 63. Both read the same line twice: a higher tax-free allowance for him, the same old freeze for her. The kettle hissed, and they did that familiar maths where you count holidays in cups of tea, not days on a beach.

*The postman had whistled when he dropped the bundle through the letterbox.*

They’re not angry, not exactly. Just winded by the logic of it — a break for pensioners, a freeze for everyone else. Two versions of April in one house. Nobody knows who to toast.

Something else is coming.

Who gets the bigger tax-free slice — and why now

For years, the personal allowance has been stuck at £12,570 while prices, wages, and the State Pension kept moving. That freeze dragged millions into paying tax for the first time. HMRC is now carving a new lane: the allowance will rise for those above State Pension age, easing the pressure on retirees whose incomes are being nudged up by the triple lock.

This is the policy’s headline: relief for people who crossed the pension-age line, status quo for everyone else. It’s neat on paper. In life, it splits households. The point is to stop routine State Pension increases tipping more pensioners into paying income tax on modest private pensions or savings. It also nods to something quietly true: retirees don’t pay National Insurance, so their “take-home” moves differently.

Picture Irene, 71, with a full State Pension of about £11,500 and a small private annuity paying £2,100. Under a frozen £12,570 allowance, most of her private pension could be swallowed by tax. With a higher pensioner allowance, more of that small top-up stays in her pocket. Not a windfall, but a weekly shop with fruit that isn’t on offer.

Or think of Alan, 67, working two days a week at a garden centre and drawing £8,000 from a personal pension. He pays no National Insurance, and the new allowance gives him extra headroom before the 20% band bites. That might be the difference between replacing a boiler now or nursing it through winter. We’ve all had that moment when a bill decides what your month will be.

The logic behind the move is straightforward. The State Pension keeps rising under the triple lock, and more pensioners were drifting into tax simply because thresholds stayed put. By lifting the allowance for pensioners, HMRC tilts the scales back a touch. It protects the idea that the basic pension shouldn’t stealthily become taxable for those on low to middling retirement incomes. Yet the wider freeze remains for workers, which means fiscal drag still pulls pay packets into tax and higher bands. Two realities, one tax code.

There’s also an administrative angle. The State Pension is taxable, but no tax is deducted at source. HMRC tweaks the PAYE code on a private pension or job to collect what’s due. A bigger pensioner allowance reduces those awkward, back-dated corrections and those brown envelopes that make breakfast taste metallic. It’s policy with a paperwork dividend.

What to do this tax year to actually feel the change

Check your tax code the moment your pension provider or employer updates it. If you’re over State Pension age, your personal allowance should show the higher number. The State Pension will likely be offset in that code, so your private pension or part-time job shoulders the tax. Log into your Personal Tax Account, compare the figures, and correct anything that smells off with a quick digital nudge. Small fixes stop big headaches later.

Think about the order you take income. Many retirees pull first from cash, then from pensions, then from investments. Flip that if it shrinks the tax you pay. Use the boosted allowance to cover part of a drawdown, and keep interest inside your Personal Savings Allowance. If you’re married or in a civil partnership, the lower earner might transfer Marriage Allowance to the higher earner — still a hidden gem for many households. Let’s be honest: nobody does that every day.

“The number one mistake is assuming the State Pension isn’t taxable,” one chartered tax adviser told me. “It is taxable — just not taxed at source. Your code has to do the heavy lifting.”

Pair that with a simple weekly checklist and you’ll sidestep the gotchas:

- Update your Personal Tax Account after any pension change.

- Ask providers for your P60s and keep them in one folder.

- Review whether interest and dividends fit inside your allowances.

- If you work, remember no National Insurance after State Pension age.

- Run a quick year-end estimate in February, not in April panic.

Common slip-ups have familiar fingerprints. Couples mix up who should hold which savings; the higher-rate payer ends up receiving all the interest. People forget to tell HMRC about a small annuity, so an over-collection arrives six months late. Others think a winter job will barely move the needle, then cross into higher-rate tax on a one-off bonus. Smoother sailing comes from knowing your bands: basic rate to £50,270, then higher rate, with Scottish bands running their own course if you live north of the border.

There’s also the question of cash flow. If you draw more from your pension early in the year, the emergency tax code can hit you hard. HMRC will usually fix it, but that takes time. Spread withdrawals, keep records, and switch one-off sums into later months if your code hasn’t caught up. Frozen thresholds mean less slack in the system, so timing is your friend.

This shift is not a free pass for wealthy retirees. Large drawdowns can still push you into higher-rate tax, and protected allowances won’t shield investment income that spills over. The real benefit skews toward modest incomes: retirees whose State Pension plus a small private top-up sit near the tax line. For them, the difference is real life, not policy chatter. It’s a taxi to the hospital instead of two buses in the rain.

If you’re still working past pension age, remember you no longer pay National Insurance on employment or self-employment earnings. That’s a quiet pay rise in itself. Combine it with the higher allowance and you might find part-time work nets more than you expected. State Pension remains taxable, but the PAYE code on your wages will usually handle it.

Now for the awkward bit. If you’re under State Pension age, nothing changes — your allowance stays at £12,570. The freeze pulls more of your pay into tax each year as wages edge up. That’s the fiscal drag story, and it doesn’t vanish with this pensioner tweak. For many workers, the only antidotes are salary sacrifice into a pension, careful use of ISA shelters, and smart use of Marriage Allowance if you can claim it. No wizardry, just solid housekeeping.

Winners, losers, and the quiet shift in the tax map

This policy double-underscores a political truth: Britain wants to protect retirees from the cold wind of tax increases that arrive by stealth. It also leaves workers to carry more of the load as thresholds sit still. Some will call it fair; others will see a generational tilt. Both can be true in the same street.

There’s a deeper cultural current. Tax in the UK increasingly happens via the back door — freezes rather than hikes, nudges rather than announcements. A bigger pensioner allowance bucks that, at least visibly. It tells retirees they won’t be punished for the triple lock doing its job. It tells workers not much at all. Policy by silence is still policy.

The practical takeaway feels small but solid. If you’re over State Pension age, the higher allowance shores up everyday spending and trims the odds of a surprise bill. If you’re younger, the map doesn’t move — but you can redraw your route. Shift savings into ISAs, test salary sacrifice, and keep a hawk’s eye on your tax code if you juggle jobs. Gains here are modest, measurable, and real.

It also reframes the family budget conversation. A couple straddling the age line now has two tax baselines. That can change who holds investments, who receives savings interest, and which pension to draw first. Set pride aside and run the numbers together. The household outcome beats personal symmetry every time.

One last thing: your local reality trumps the national headlines. If you rent, if your mortgage looks like a climb, if you support grown-up kids who boomeranged home, the way this allowance lands will feel different. Tax is personal. It only makes sense when it sits next to the bills on your kitchen table.

Wider ripples you’ll notice long after April

The bigger story is how Britain funds itself while trying not to spook anyone. A higher allowance for pensioners softens tax pressure where the political heat runs hottest. The freeze for others keeps revenue flowing without the splash of a rate rise. Over time, the tension will show up in choices about work in later life, in how savings are held, and in the quiet reshuffling of money inside families. Maybe that’s the point: incremental steps add up to a path, even if the path isn’t signposted.

| Key Point | Detail | Interest for the reader |

|---|---|---|

| Pensioner allowance rises | Above £12,570 for people over State Pension age | More income kept tax-free if you’re retired |

| Workers’ threshold frozen | Personal allowance stays at £12,570 for under pension age | Fiscal drag continues to bite pay packets |

| Practical steps | Check codes, reorder withdrawals, use ISA and Marriage Allowance | Immediate ways to avoid overpaying |

FAQ :

- Will every pensioner get a higher personal allowance?Only those above State Pension age. The uplift applies to their Income Tax personal allowance, not to working-age adults.

- Is the State Pension still taxable?Yes. Tax isn’t deducted from it at source, so HMRC adjusts your PAYE code on other income to collect what’s due.

- What if I’m over pension age and still working?You benefit from the higher allowance and you don’t pay National Insurance, though Income Tax bands still apply to your earnings.

- Does this help if I’m a higher-rate taxpayer in retirement?It reduces the slice taxed at 20% first. If your income goes beyond the higher-rate threshold, higher-rate tax can still apply to the rest.

- How do I check my tax code is correct?Use your Personal Tax Account online, compare it with provider letters and P60s, and request a correction if something looks off.

So HMRC lifts the allowance only for those above State Pension age—how is that fair to workers whose pay is already dragged into tax by frozen thresholds? It feels like stealth redistribution by age rather than need. Any impact assessment on intergenerational equity?

Two Britains, two kettles hissing—love that line. In our house it’s ‘cheers’ to Mum and ‘sorry’ to Dad. Guess who’s 66? 🙂 Also, who explains this at Sunday lunch without starting a row?